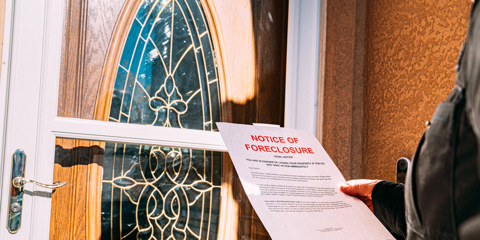

The California Association of REALTORS® (C.A.R.) declared “victory” upon the Senate passage of SB 1178 on June 3, 2010 (the bill now moves to the Assembly for approval). Should this bill become law, California real estate agents should be cautioned to read the legislation very carefully because the protections afforded will be very narrow in scope.

We already know that California Code of Civil Procedure (CCP) Section 580b prohibits a lender from seeking a deficiency judgment after the foreclosure on a “purchase money” loan. A purchase money loan is a loan that was used to acquire an owner-occupied residence. Most borrowers do not understand that when they refinance a purchase money loan, even if just to get a better rate and term, they lose the anti-deficiency protections of CCP 580b.

As C.A.R. explains in its “RED ALERT” announcement, SB 1178 is meant to extend the anti-deficiency protections found in 580b to homeowners who have refinanced purchase money loans and are now facing foreclosure. What is left unsaid from the announcement is that the protections in the proposed law are limited to the amount of the original purchase money loan. Therefore, borrowers are still exposed to deficiency claims for any “cash-out” portion of the refinancing. It is this cash-out portion of the refinancing that is creating the extensive deficiency exposure faced by many California borrowers.

If this bill is signed into law by the Governor, we should be careful not to overstate of the victory, as was done upon the passage of the Mortgage Forgiveness Debt Relief Act of 2007 (borrowers were being told that all cancellation of debt was tax-free – this is simply not the case). While SB 1178 will produce a very good law, it will not be a panacea for the aftermath of California’s refinance boom.